Yesterday's retail sales were better than expected and jobless claims show no signs of labor weakness, yet rates continued their post FOMC decline. The BoE and ECB both sounded more hawkish than the FOMC. Yields continue to fall further to start the day as the everything rally continues. 2Y at 4.39% and 10Y at 3.92%.

ATL GDP now is at 2.6% for 4Q. Empire Mfg and Industrial Production on the day ahead.

XTOD: Holiday Video (Blackstone's Version) 🎬🎵 Inspired by the Eras Tour, Steve Schwarzman & Jon Gray take $BX on the road for “The Alternatives Era” Tour… many sequins & one original song later, we bring you the latest in our annual tradition ⬇ Watch the full video: https://bit.ly/47V13YZ

XTOD: I watched this again and I’m 80% sure it’s going to be in a documentary ten years from now about a massive financial crisis

XTOD: “Not only will we not tell you the accurate marks, but we’re hilarious!” Aside from the cringeworthy video, can we please stop calling highly correlated levered equities “alternatives” because they don’t update the prices? That doesn’t make them bad investments, but they ain’t alternatives.

XTOD: Powell has no problem with money going into stocks. It cant do any (inflation) damage there, and the capital gains tax revenues will be welcome. He needed to get the "pivot" (which, unlike the Put, was always inevitable) out of the way before Iowa. Now they go dark.

XTOD: Criticize the Fed on policy grounds, but trade with them, because they are bigger than you.

I do both :)

XTOD: Here's a great stat for you: The small-cap Russell 2,000 made a new 52-week high today after hitting a 52-week low just 48 days ago. That's the shortest turnaround time in the index's history to go from 52-week low to 52-week high dating back to the 1970s!

XTOD: A quick 🧵on monetary policy because I see a lot of market commentators who don’t seem to understand what the Federal Reserve is thinking regarding the future path of interest rates. One way to think about monetary policy is in terms of the difference between the policy interest rate and the “natural” interest rate. The conventional wisdom in the mainstream of the profession is that when the policy rate is below the natural rate, inflation rises. When the policy rate is above the natural rate, inflation declines. When the policy rate is equals natural rate, the inflation rate is constant. If you accept this premise and you are in a world of rising inflation, that means the policy rate is too low. But you can’t just raise the policy rate to equal the natural rate since you need inflation to decline. Thus, you have to raise the policy rate above the natural rate. Of course, you can’t leave the policy rate above the natural rate indefinitely. Thus, once inflation comes down and expectations of inflation start to be around the central bank’s target rate, they should lower the policy rate down to the natural rate. Thus, there’s no great mystery about why the Fed is signaling that rates will be lower next year. This isn’t the Fed admitting there are fiscal constraints. This isn’t the Fed having weak hands. This isn’t (necessarily) an Arthur Burns moment. This is their standard framework. Now, it’s possible that they lower rates too soon. That could be — or might lead to — an Arthur Burns moment and the potential for the stop-go policies of the 70s. But the main challenge the Fed is going to face in the months ahead is how it weighs its credibility with the public against what their policy framework would say to do. They might be reluctant to lower rates if the public sees them as lowering rates too soon. Thus, if they lower rates too soon, inflation won’t get back to 2%. If they are perceived to have lowered rates too soon, this affects their credibility & inflation expectations could be wildly un-anchored. If they wait too long to lower rates, they’ll likely cause a recession To me, this suggests that all the talk about a soft landing are wildly pre-mature. (A lot of this is just cheerleading anyway.) This is especially true because a lot of debt is going to have to roll over at higher rates in the coming months. But my basic point is that a lot of the commentary following the Fed meeting is just noise. It’s straightforward to understand what they’re doing if you know how they think.

The FOMC meeting (recap here) lead to an everything rally as the Dow hit a new record high and the 2Y Treasury yield plunged 20bps and yields were lower across the curve, sending bond prices higher. The everything rally continues this morning with yields down 8-13bps, the 2Y right around 4.30% and the 10Y under 4% to 3.95%. Do you recall, not long ago, in late October when both the 2Y and 10Y were over 5%, hard to believe. There was also lots of speculation on hedge funds facing large margin calls yesterday leading to forced selling of Mag7 stocks as the FOMC meeting hit.

If you're in the soft landing camp, do you have a definition of that term? If you need one, I find Scott Sumner's description worth a read it's part of his full post here:

"Mark your calendars. Unemployment fell to 3.6% in March 2022. Now it’s 3.7%. If it’s still relatively low in March 2025, and if inflation has fallen close to the Fed’s 2% target, then the US will have achieved its first ever soft landing. Three years of cyclically low unemployment without triggering high inflation is something that has frequently occurred in other countries (say the UK in the early 2000s), but never in the US. No one knows why.

America’s been around for a quarter of a millennium, which is a long time. The early years are not well documented, but I’m pretty sure that we’ve never had a soft landing since at least the Civil War. And yet it seems like Wall Street prognosticators are increasingly of the view that the US will soon achieve a soft landing, our first ever."

On the day ahead, don't worry you have more Central Bankers (the Swiss already left rates unchaned, the ECB and BoE are still to come) along with retail sales data.

In other news, House Republicans voted to authorize an impeachment inquiry into Biden.

In still other news, researchers at the BIS stumbled upon this novel idea "Hedging interest rate risk can reduce firms’ exposure to higher interest rates whenever they hold variable rate debt." I know it sounds crazy that hedging, which is designed to reduce risk to higher interest rates, will reduce risk to higher interest rates. I thought it seemed inherent or somewhat definitional in the term "hedging", but I feel much better now knowing that researchers have agreed.

XTOD: Ah cuts in January now nearing a coin flip. Makes complete sense

XTOD: It’s almost like Jay Powell thinks inflation was reduced by the Fed’s large and sudden increase in interest rates rather than by pandemic recovery, and now that inflation has been lowered by monetary policy he has to ease up slowly to get down to 2% target and not overshoot.

XTOD: Not to beat too much the same drum, but a one-time fiscal blowout leads to inflation that comes from nowhere (if you're Fed) and goes away on its own. Fed can jump in front of parade & help a bit. Until the next fiscal blowout. Model simulation of a fiscal shock:

XTOD: It makes sense to look at the post C-19 inflation as a "bribe" perpetrated by the Fed!

XTOD: This is exactly how you embed secularly higher inflation expectations and lose your credibility as an institution. The asymmetry is the message...Mistake is sort of a loaded term. If the era of secular low inflation is back it's very clearly the right move. But if it's not then it will prove to have been a mistake. IMV the balance of risks means being concerned about embedded inflation still dominates, for me.

XTOD: The remaining above-target inflation is mostly cyclically-driven (i.e. caused by excess aggregate demand pressures). This is why I suspect the “last mile” of returning to 2% inflation is going to be more challenging than the happy-go-lucky disinflation we’ve had so far. https://shorturl.at/aegsE...Chair Powell agrees: “While the broader supply recovery continues, it is not clear how much more will be achieved by additional supply-side improvements. Going forward, it may be that a greater share of the progress in reducing inflation will have to come from tight monetary policy restraining the growth of aggregate demand.”

XTOD: Forecasts of 3% 10 year in 2024 are farcical. If Fed funds rest at 3% then 10 year average term premium of 1.1 indicates at 4% that we are there.

XTOD: Test scores are plummeting worldwide. Why? Probably because of phones. We should ban phones from the classroom.

XTOD: Buster Posey: SF Giants Lost Shohei Ohtani to Drug, Crime Issues Buster Posey, now part of the Giants' ownership group, said players and their wives feel uncomfortable about the state of San Francisco.

As expected the FOMC remained on hold for the third straight meeting, leaving the Fed Funds Target range at 5.25% to 5.50% with no changes to QT or other policies.

The language in the FOMC Statement was less firm on the possibility of additional rate hikes.

The Dots showed the Fed forecasting a 50bp lower 2023 Core PCE rate relative to estimates from September, as well as a 50bp reduction, from 5.1% to 4.6%, in the Median 2024 Fed Funds dot relative to September.

Powell indicated the Fed remains fully committed to returning inflation to 2% goal, characterizing the current stance of policy as restrictive and cited the long and variable lags associated with monetary policy.

Powell indicated that FOMC participants believe we are at the peak of interest rates.

"Normalization Cuts" were discussed in the press conference, albeit poorly, but Powell acknowledged there was discussion as to when to start cutting rates as inflation cools.

2Y yields were down 20bps following the FOMC Statement and fell a further 10bps as Powell spoke, breaching 4.45%.

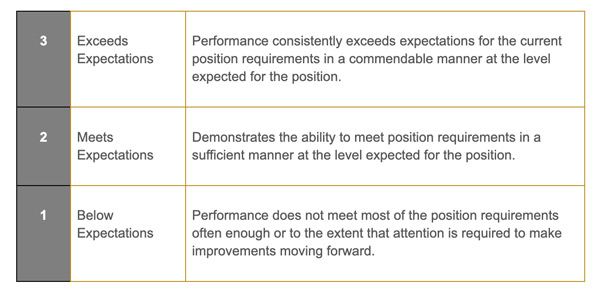

Every year most of us are forced to write down our professional goals, usually cascading down from company and team goals to you as the individual. Now is that time of year where many organizations are conducting their performance reviews. With that in mind, there is no better time than now to review the FOMC's performance for this year.

As is the case with any good performance appraisal, you should start with some objective criteria against which you are measuring performance. In the case of the FOMC, Congress specified the goals of the Fed as: (1) maximum employment, (2) stable prices, the so called "dual mandate", but there is an often forgotten third mandate in the amended Federal Reserve Act of 1977 and that is (3) moderate long-term interest rates.

Now for the appraisal:

On Maximum Employment - Exceeds Expectations: we came into 2023 with forecast for recessions which would have included job losses. The unemployment rate remains below 4% and though there may be some signs of labor market weakness, it's hard to say that the jobs picture isn't more robust than what most expected at the start of the year.

On Inflation - Needs Improvement/Below Expectations - you can argue with me until you are blue in the face that the Fed deserves a better grade here given the rapid disinflation seen in PCE and CPI data, but perhaps an example will sway you. Assume that you, as an employee, start the year with your boss telling you that the number of errors (maybe it's trading errors, maybe it's quality defects) you made was way to high last year and that the number of errors to be tolerated was 2. Your boss gave you a second chance last year because they knew there were some extenuating circumstances and you hadn't made too many of these types of errors recently, so your boss let you overshoot the error quota for a while (your boss even allowed you to change your the policy goal to "FAIT"), but said they weren't going to tolerate errors above 2 forever. You go into 2023 knowing you have to bring the level of errors back to 2, so you continue to be aggressive with your policies, they seem to be working, but your errors are still double what you were told you needed to achieve. Well, that's the Fed, they have that 2% inflation goal, but we're sitting here today a year later and we're still nearly double that rate. You wouldn't get away with that in your performance review, would you? You can tell your boss that everyone thinks your error rate will come down in the future, expectations are that they will, but would your boss keep giving you a pass?

On Moderate Long-Term Interest Rates - Meets Expectations - in the Federal Reserve's publication, "The Fed Explained: What the Central Bank Does" it states: ".. long-term interest rates remain moderate in a stable economy with low expected inflation...". This third mandate is never really mentioned because it seems to be dependent upon the first two topics. Certainly yields are higher than some people expected as the start of the year and they seem more moderate than they were when most of the curve was very low across the curve in the 2010's. But with so much uncertainty around things like R* and U* it's hard to do better than "meets" here. I think the Fed did a better job on meeting or exceeding "volatile" long-term interest rates this year than they did on meeting the definition of "moderate". Arguably the rating could be worse as the Fed seemed to be relying upon tightening of financial conditions to do some work for them, with that tightening coming from higher long-term rates, and that seems to be going the wrong way as financial conditions have eased into year end.

Most reviews also include a section where the manager provides some narrative assessment of how things are going for the employee being reviewed. Here's mine for the Fed:

While progress has been made towards your goals, it's unclear how much of the success is attributable to your performance. You haven't done a great job of explaining your reaction function and often the market discounts what you are saying and believes you'll abandon your goals early if they complain loud enough. What is your reaction function? Are there rules you look at and follow to help you achieve your goals?

Your colleagues noted you did a lot of talking and many times that talking was distracting. We value a high "sit-next-to" factor here and it seems you can cause a lot of people anxiety. It seems like you spend most of your day just talking, when do you get work done? Oh, I see you think your job is mostly talking, propaganda, and suasion. We'll take this under consideration in 2024 goal setting.

Your track record of forecasting is not good. In 2024 maybe you should focus on the concept of "Margin Of Safety". In the words of Benjamin Graham in his classic book "The Intelligent Investor", Margin Of Safety is "in essence, that of rendering unnecessary an accurate forecast of the future". I know you're trying to balance both risk to unemployment and inflation, but look at where you need improvement, perhaps you might need to apply the Margin Of Safety concept to your inflation mandate.

Lastly, your performance was mixed on supervising your direct reports. Remember how several banks failed? You did a nice job of limiting the impact, but some find it troubling how this happened in the first place and how you seemed to miss the build up of economic and financial risk in years prior as well.

As we head into 2024, as you stay employed in your job of steering the most important economy in the world, I will remind you of some advice from the late, great Charlie Munger, "Nobody survives open heart surgery better than the guy who didn't need the procedure in the first place." You say you'd rather be Volcker than Burns, your goal for 2024 is to get inflation back to 2%. Let's try to get there without breaking something that will require open heart surgery.

Another FOMC decision day is upon us. Check back around the 3pm hour for my summary and related commentary. I'll be giving the Fed their annual performance review. Yields down slightly to start the day with the 2Y at 4.73% and the 10Y at 4.19%. Yesterday's CPI showed inflation slightly higher than expected, but economist will debate the continued stickiness of shelter related inflation while they seem confident on continued goods disinflation. The 30Y treasury auction seemed well received.

This morning's UK GDP data showed economic contraction and EU industrial production data looked weak. I won't comment on Argentina, but seems like newly elected President Milei is starting his radical overhaul of the economy.

On the day ahead we get PPI data ahead of the 2PM FOMC decision which includes the Summary of Economic Projections (aka the Dots). Will Powell push back on the easing of financial conditions? How many cuts is the FOMC dot plot showing? We'll soon see.

XTOD: Core PCE is 4.0% and markets party like it's 1999.

XTOD: H4L baby

XTOD: I realize some of my views might seem contradictory so let me try to clarify a little:

-I expect very gradual weakening in the labor market and don't think the Fed should cut until it's clear the risk a resurgence of inflation is behind us

-While I think the Fed shouldn't cut, I think they will, because they have a significant institutional bias toward inflation (and political bias as well) (this is longer term - I Don't expect signals of cuts tomorrow, quite the contrary)

-I think the decline in inflation this year is quite brittle and vulnerable to a reacceleration if wages pick back up, which will happen if the labor market doesn't get a little more slack in it

-The Treasury is conducting monetary policy and using its reduction in coupon issuance to interdict Fed QT

-There are upside risks to fiscal expenditures if the side deals from the FRA negotiations in the spring get implemented, i.e. if the House gets railroaded by the Senate. The Biden Admin continues as well to come up with new and creative ways of inflating the costs of the IRA to get more fiscal $ out the door as fast as possible

-That easing of policy from Treasury (and accompanying loosening in fincon) continues to run the risk of reacceleraiton in growth and thus inflation

-If the Fed hadn't made the critical errors it did in '21/'22, it would be a no-brainer to have cut six months ago. But history matters, and affects the risk of future inflation, and we are where we are

XTOD: Job satisfaction in the US is at a 35-year-high. In 2022, over 62% said they were of people said they were satisfied with their jobs, up from < 45% in 2010. Big gains come from work/life balance and the performance review process.

XTOD: I’ve seen what you describe. Growing aggressively to $100mm, and all of the sudden growth slows. It’s really painful.

In my experience, the number one reason this happens is fear of change. What ever set of variables led to the product/market fit that took you to $100mm become sacrosanct. These “sacred cows” become limiting constraints which hold you stuck on a local maximum. Growth goes from 30% to 20% then to 11% or even 8%. And product tweaks or pricing tweaks that you have discussed for over 5 years just can’t find their way to the market. Everyone is afraid those changes will hurt things. But you are already decaying.

CPI day in 'merica. Markets are looking for a 0.3% mom and 4% yoy in the Core rate and a 0.00% mom and 3.1% yoy increase in the headline inflation print. Guess we'll see.

Yields start the day down 4bps after rising yesterday.The 2Y is yielding 4.68% and the 10Y is 4.18%. The two treasury auctions yesterday tailed and on Twitter/X, Andy Constan graded the 3Y as a D and the 10Y as a C-. Today we get $21 billion of 30Y treasuries auctioned today.

I'd wager that more ordinary people will learn about the Time Value of Money because of Shohei Ohtani's contract than from any formal education program. When you have sports writers like Jeff Passan writing this: "The deferrals also affect the net present value of the deal. There’s a rule of thumb across all walks of life: Money today is more valuable than money tomorrow, inflation being what it is. When you defer money, you’re taking less. The Dodgers are operating in an environment in which the prime rate is 8.5%. And with money today being so pricey, it lowers the present-day value of the deal by a significant margin." and Fabian Ardaya writing: "The deferred money is to be paid out without interest from 2034 to 2043."

XTOD: Let me get this straight: The Los Angeles Dodgers are proposing to pay the most talented baseball player in history like he's a mediocre middle reliever while he plays for the team ... and then create a retirement annuity that pays him more than any other active player.

XTOD: Our #CPI indicator updates tomorrow. Our #inflation nowcasting model (updated daily!) predicts year-over-year CPI #inflation of 3.04% in November. Check it out: http://clefed.org/3yCkTHV

XTOD: A whole generation appears to think you can copy other’s exact words without using quotation marks as long as you acknowledge the source. That’s as good a proof as any that our universities aren’t up to snuff.

XTOD: WeWork founder Adam Neumann's new start-up, Flow, will officially launch their first property early next year according to the Business Insider According to various reports/articles, it looks like a classic apartment management company w/ an app...

It'll be interesting to see if there's a unique tech angle that'll explain why Andreessen Horowitz (a16z) invested $350 million into the company

XTOD: If you don't understand the unit economics of a business you are a damn fool. What's the value of an average customer considering: what they cost to acquire, how much revenue they produce per month, how long they pay and how much they cost to serve. It's not rocket science.

XTOD: Charlie Munger’s biggest takeaway from William Green’s book, “Richer, Wiser, Happier” - a lot of the mentioned great investors got divorced. A deep reminder that as much as we tend to be high focused and consumed with our work, and that it demands up to be unemotional with our decisions.

We need to flip this switch off when it comes back to our love ones. It’s the abundant life and in moderation to be able to really savor life that matters.

XTOD: After a long year, it's finally time. Announcing the Worst Tweets of 2023 Bracket! I've spent the entire year collecting hundreds of deranged tweets, awful takes, and the most insane discourses on this site. Only 64 were chosen. Now it's time to crown a champion. The rules:

* No Elon Musk. It's too easy and would end up being half the bracket.

* We're not just looking for regular bad. We're not looking for normal slapfights.

* We're looking for that special brand of insanity you only get on twitter.

The field of 64 is divided into four regions named after some of our greatest discourses: the Bean Dad region, the Coffee Wife region, the Chili Neighbor region, and a special Israel/Palestine Containment Zone. Voting threads are below! May the worst tweet win!

Jobs Friday faded into what I’ll call Shohei Saturday with Ohtani getting a record $700mm, 10 year deal. If the Dodgers market him correctly, maybe he’ll create a Taylor Swift economic boom? We need more excuses for economic growth and inflation.

The 10Y starts the week at 4.26% and the 2Y at 4.75%, both up from where they started the day Friday as Friday's jobs numbers seemed to cause a reassessment of the pace of rate cuts that the market had priced into the curve. If you're looking for a summary of Friday's jobs report, perhaps the best read on Friday's jobs number was this take from Barry Ritholtz per his blog post here: "You may have missed the most important data point in today’s Employment report. It wasn’t that Nonfarm payrolls increased by 199,000 in November, somewhat higher than expected; nor was it the unemployment rate, which fell to 3.7% in November, from 3.9% in October; nor was it that Wages continued to rise at a modest pace, with average hourly earnings up 0.6%. It was that 157.087 million people are employed full-time in the United States.... First, it is a full 5 million more people working today than in January 2020, just before the pandemic struck."

In other news, the UofM survey sure seems to really be correlated with gas prices, gas prices down sentiment up and inflation expectations down.

The week ahead features the some major Treasury auctions, CPI, Retail Sales, FOMC, BoE and ECB. The main action with this week's FOMC will likely market participants scrutinizing the number of cuts implied in the "Dots" and if there are any changes to where the Fed believes the long-run neutral rate is estimated. The other term you'll probably become familiar with, or hear more of this week, is "normalization cuts". These are rate cuts that are necessary to keep the real interest from becoming overly restrictive as inflation falls

On the week ahead:

Monday: NY Fed survey of consumer inflation expectations, 3Y and 10Y Auctions Tuesday: CPI, 20Y auction

Friday: is it the weekend yet? It's been a lot of central bank meetings to hear about

XTOD: 'Even if inflation declines, soaring debt levels, deglobalization, and populist pressures will keep rates higher for the next decade than they were in the decade following the 2008 financial crisis.' https://project-syndicate.org/commentary/era-of-low-interest-rates-has-come-to-an-end-by-kenneth-rogoff-2023-12 by @krogoff

XTOD: Here’s what the economists don’t get about the vibes in the economy. People hate inflation. Inflation turns the economy into a war of all against all. When the government prints and spends money it in turn raises the price level and creates winners and losers. One then has to expend effort in order to not become a loser. Asking for raises, switching jobs, speculating with savings etc. it requires a lot of effort and frankly feels dishonest because it is in fact somewhat dishonest. Savvy, lucky and advantaged people come out ahead while less savvy, less lucky and disadvantaged people fall behind. That is why people hate the economy - despite the average being the same the distribution is different and redistributed in a way that feels arbitrary. As Keynes puts it “The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.”

XTOD: Hey, I thought Biden always said he respected the Fed’s independence. What gives?

“Biden said the Federal Reserve should be discouraged from raising interest rates, in rare comments from the president on central bank policy making” https://bloomberg.com/news/articles/2023-12-08/biden-says-jobs-numbers-should-deter-more-fed-rate-hikes?utm_source=website&utm_medium=share&utm_campaign=twitter via

@bpolitics

XTOD: If you change your mind too frequently, it suggests that you do not think carefully and responsibly before formulating an opinion & don't know when to remain silent or neutral.

If you never change your mind on anything, it indicates that you are an intellectually dishonest.

XTOD: The Media Is Hyping Up "Carbon Passports" To Restrict Travel

XTOD: Curb Season 12...February! “Curb Your Enthusiasm” Season 12 will return to HBO in February. Network CEO Casey Bloys announced the premiere month during a Thursday media event in New York.

XTOD: NEW: President Joe Biden announces a remarkable "billion 300 million trillion 300 million" dollar infrastructure plan. I'll admit, that's impressive! In the same breath of saying Donald Trump doesn't know what he's talking about, Biden appeared to claim that America is having an "infrastructure decade" with a price tag of "over a billion 300 million trillion $300 million dollars." Very cool!

XTOD: $700 Million: What the Dodgers just agreed to pay Shohei Ohtani. $667 Million: Total Oakland A's Payroll, Last 10 Seasons

XTOD: Time, diversification, and compounding are the only friends you’ll ever make in investing.

XTOD: Steve Jobs on leadership “The greatest people are self-managing. They don’t need to be managed. Once they know what to do, they’ll go figure out how to do it… What they need is a common vision, and that’s what leadership is. Leadership is having a vision, being able to articulate that so the people around you can understand it, and getting consensus on a common vision.”

Jobs Day in 'merica. Will the jobs report throw cold water on the recent bond rally and bets for rate cuts or will it lend further credence to the 'lower faster' yield camp (who might also be the 'Fed put' camp)? The impact of the return of striking auto and SAG workers may complicate the interpretation of the data where expectations are in the +180-190K range, though the unemployment rate might be the more important number. It's comical how many economist are discussing the triggering of the Sahm rule, often to the extent of ignoring or disagreeing with Claudia Sahm who created the rule. Yesterday, Claudia put out a post with all the steps involved in the calculations for the rule she created.

Yields are up 4-5bps to start the day with the 2Y at 4.63% and the 10Y at 4.18%

Yesterday's jobless claims data didn't show any signs of a deteriorating labor market. On the equity side, Google and AMD said something, something, followed by the magic word "AI" and their shares went up, taking the market with them.

You probably missed the release of the Treasury OFR's Annual Report to Congress on their assessment of risks to the U.S. financial system and economy. The headline takeaway was "Financial-stability risks have increased since last year’s report and remain elevated in 2023. Multiple indicators signal an upcoming economic slowdown—potentially magnified by persistent inflation, ongoing geopolitical risks, and global conflicts." If you want a summary of their research on various areas of financial risk, you can find it here

XTOD: Just because you have free time doesn’t mean anyone who asks for it is entitled to it.

XTOD: Can Social Security Be Saved by Selling America’s Oil & Gas Reserves?

The proposal: In a town hall hosted by Fox News, former President @realDonaldTrump

suggested that America’s fiscal problems – and specifically #SocialSecurity’s looming insolvency – can be solved by tapping into the “incredible wealth under our feet” in the form of domestic oil and gas.

Our findings: Dedicating current oil and gas leasing revenues to Social Security would cover less than 4 percent of its shortfall, and it would be impossible to fix Social Security even if all federal land were opened to drilling operations.

XTOD: An amazing roller coaster ride for the 10-year treasury yield, despite no meaningful change in expected future primary budget deficits.

XTOD: An income-based explanation for "vibecession": 1) Even though we haven't had an actual recession over the past 2 years, inflation-adjusted personal income per capita (blue) have behaved in a recessionary way. 2) That's true even though "the economy is good" (orange)

XTOD: Blackstone, Digital Realty join hands to develop $7 bln data centers http://reut.rs/4aecEE3

XTOD: The Department of Justice on filed new criminal charges against Hunter Biden, US President Joe Biden's son, accusing him of failing to pay $1.4 million in taxes while spending millions of dollars on a lavish lifestyle https://reut.rs/3uLvAJX

XTOD: After this week’s unacceptable testimony from presidents of @Penn

@Harvard , and @MIT , the Education Committee is launching an official Congressional investigation that will include substantial document requests and compulsory measures including subpoenas to those universities and others. 🚨🚨🚨 https://stefanik.house.gov/2023/12/stefanik-statement-on-committee-on-education-the-workforce-announcing-investigations-into-mit-harvard-penn-following-their-inability-to-condemn-antisemitism

XTOD: On December 7, the #GDPNow model nowcast of real GDP growth in Q4 2023 is 1.2%. http://bit.ly/32EYojR #ATLFedResearch

XTOD: I'm still a bond bear. I still have my target of 5.50% 10-year in 2024. I'm in the "no landing" camp. That is no recession or even a soft landing but continued expansion. (as an aide, I've been critical of the soft-landing forecasts as they don't have an accepted definition, and by some criteria, it can be argued there has never been a soft-landing before). So, I think there will be 2+% real GDP growth in 2024. I'm also in the "sticky" inflation camp that bottoms at 3+% in the long run, not 2% (it only gets to 2% in a full-blown hard landing or recession, which I do not see).

For both above, I've argued the cycle changed in 2020. The labor market is very different (remote work) and more transactional. That means employees are more willing to quit (or strike) as they are fearless in finding another job. This confidence allows them to keep spending.

So 2+ real GDP growth and 3+% inflation = 5+% nominal GDP, which is how I get to 5.50% 10-year in 2024.

A word about what this means for risk assets, like stocks: they will see the headwind of a viable alternative ("TINA" died in 2020). This was the case in 2023 with everything but the "Mag 7" stocks struggling to beat cash ... for the second year in a row.

Dr. Jeremy Siegel has a new edition of his book "Stocks for the Long Run" this year. In summary, the long-term potential of the stock market is now 8%. If investors can continue to get 5+% from the bond market, why take the extra risk of 3%?

On this front, the era of buying indices is now over. Peter Lynch can come out of retirement as we are on the road to transitioning back to a stock-picking environment.

XTOD: Essentialism isn’t about getting more done in less time. It’s about getting only the right things done.